Homeownership is a major financial commitment, and the terms of your initial loan rarely stay a perfect fit forever. Life brings changes, markets fluctuate, and your financial goals naturally evolve over time. You might start wondering if adjusting your mortgage could offer some relief or open up new opportunities.

Refinancing your mortgage involves replacing your current loan with a new one to potentially lower your monthly payments and access home equity, but it also carries drawbacks like legal fees and a longer repayment timeline. Look at your current interest rate, review your household budget, and decide if a new product aligns with your plans.

Top Benefits of a New Mortgage

Securing a new home financing contract can offer several distinct advantages that directly improve your everyday financial situation.

Lower Rates & Smaller Payments

Review your current interest rate and compare it to current market offerings. Securing a better interest rate remains a common reason homeowners seek new terms.

A new contract can help you secure a better interest rate for your property. This change can help lower your monthly payment amount so you keep more money in your personal bank account. You can then free up cash for other bills instead of giving it to the lender. An extra few hundred dollars a month can help cover groceries or car repairs easily.

Cash Out Your Home Equity

You can turn the built-up value of your property into usable cash right now with home equity loans. This approach can help you pay off high-interest credit card debt fast. You can also use these funds to fund large home renovation projects. A new kitchen or a finished basement can make your daily routine much more enjoyable and potentially increase your property value over time.

Change Your Loan Structure

Your current terms might no longer fit your daily life. A refinance lets you switch from an unpredictable variable setup to a stable fixed rate. You can sleep better knowing exactly what your payment looks like every single month. A refinance also allows you to make structural adjustments to the title and contract. Use this process to:

- Remove a former partner from the property title

- Add a new spouse or co-signer to the mortgage

- Change your payment frequency

- Consolidate a secondary loan into your primary mortgage

The Potential Drawbacks & Extra Costs

Breaking a legal contract naturally introduces new expenses and potential delays that you need to consider before signing any paperwork.

Final Fees & Legal Costs

Breaking a contract often triggers several closing charges. You should expect to spend money out of pocket to set up the new terms. Common costs you might encounter include:

- Prepayment penalties for breaking your term early

- Real estate appraisal fees

- Mortgage discharge fees

- Legal and title transfer fees

Calculate these fees carefully to ensure the long-term savings outweigh the immediate financial hit.

A Longer Repayment Timeline

Starting a new term means you reset the clock on your loan entirely. This extension can spread out your payments over many more years, which might lower your immediate monthly obligation but increases the total interest you pay over the life of the loan. Factor in your ultimate payoff date and decide if you feel comfortable carrying debt further into the future.

A Temporary Credit Score Drop

Lenders review your financial history before approving new terms. This process requires a hard credit check, which temporarily lowers your overall rating. Protect your credit in the months leading up to a new application by paying all bills on time and avoiding new consumer debt.

When a Switch Is a Good Idea

Timing plays a crucial role in deciding whether to stick with your current lender or move to a completely new mortgage product.

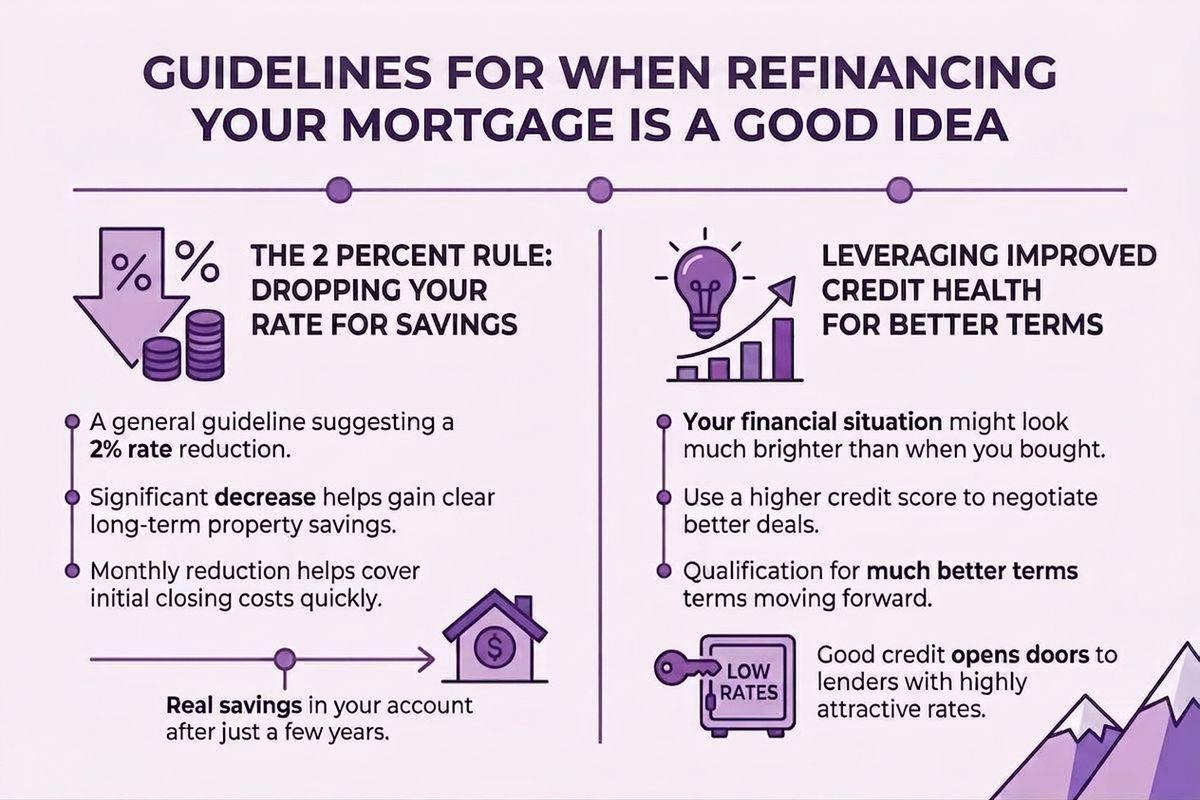

A general guideline suggests dropping your rate by 2 points. This significant decrease can help you gain clear long term savings on your property. The monthly reduction can help cover the initial closing costs quickly. Run the numbers to see exactly when you hit your break-even point and start seeing real money stay in your pocket.

Leverage improved credit health to negotiate better deals. Your financial situation might look much brighter today than when you first bought your home. You can leverage a higher credit score to negotiate better deals. This improvement can help you qualify for much better terms moving forward. Good credit opens the door to lenders who offer highly attractive rates.

When to Keep Your Current Loan

A tiny decrease in your interest rate rarely makes sense for a complete structural change. The heavy final fees cancel out small interest savings almost immediately. The basic math does not support the switch when the margins look this thin, as you might spend thousands of dollars just to save 10 dollars a month.

Changing your terms makes little sense if you want to sell your property in the near future. You might move before you break even on the new setup costs. This timeline can force you to pay unnecessary final fees for no real benefit. Keeping your current setup can help you avoid these extra closing charges entirely.

Take Control of Your Financial Future Today

Finding the right path requires careful comparison and clear numbers. You can compare different lenders & rates easily with help from an experienced mortgage broker. You deserve to understand every detail of your property financing without any confusion. Secure transparent loan advice to build a strong plan and keep the focus exactly where it belongs.

Reach out to Mortgage Connection today to explore your options and find the right mortgage solution for your needs.