Maybe you’re about to reach the end of your renewal term, and you’re wondering if you can finish paying off your mortgage and pop some champagne. We know how confusing mortgage contracts can feel, so when you finally reach the end of your payment term, our team at Mortgage Connection can help clarify the rules for your remaining balance.

In many cases, you can pay off your mortgage in full at renewal without prepayment penalty fees, provided the payout happens at the end of your term. Learning how mortgage renewals work can help increase your confidence and take control of your financial future.

How Mortgage Term Renewals Work

The End of the Term

At the end of your mortgage term, your mortgage can be paid off, renewed, or changed without prepayment penalties. During that time, lenders allow you to make large payments without charging any extra money. You just need to confirm the precise date with your lender to help avoid surprise charges.

Open Versus Closed Mortgages

There are 2 kinds of mortgages, open and closed. Open loan types let you put down extra cash whenever you want, but they often come with higher interest rates. Closed mortgages usually come with lower interest rates, but they often limit how much extra you can pay toward the mortgage before your term ends.

You can talk to our mortgage brokers in Calgary to help review the specific details in your contract.

Options for Your Balance at Renewal

Full Balance Payment

This option allows you to pay off the entire remaining loan balance with a single payment. This move turns you into the full owner of your home, so there will be no more monthly mortgage payments to factor into your expenses.

Large Lump Sums

You might want to drop a chunk of savings onto your principal balance before you sign papers for a new term. This strategy reduces the amount you still owe, allowing you to enjoy much smaller monthly payments.

Debt Consolidation Options

A renewal provides a chance to use your home equity to pay off outside credit cards or car loans. Some homeowners choose to consolidate higher-interest debts into their mortgage at renewal, depending on their available equity and lender approval.

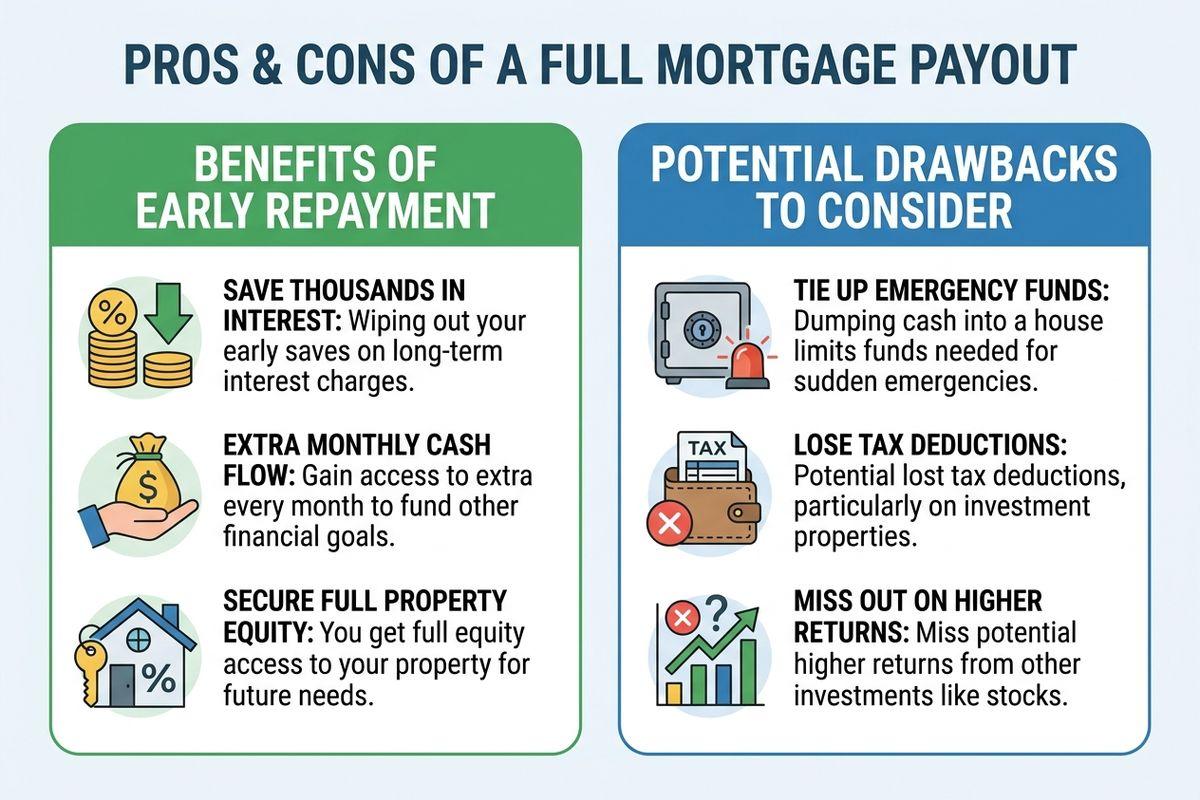

Pros & Cons of a Full Payout

Benefits of Early Repayment

Finishing your loan early can help you save thousands of dollars in long-term interest. When you pay off your mortgage, you suddenly gain access to extra cash every month to fund different financial goals. You also own your property outright once the mortgage is fully paid off.

Potential Drawbacks to Consider

Paying off your mortgage in full can be a huge milestone, but it’s still important to think about your overall financial picture. Using most of your savings to clear your balance could leave you with less flexibility for emergencies or future investments. In some cases, paying off a mortgage on an investment property may also affect certain tax considerations, so it’s often a good idea to talk to your mortgage broker about what aligns the most with your financial goals.

Important Considerations at Renewal Time

Preservation of Emergency Funds

It’s widely recommended that you should always keep 3 to 6 months of regular living expenses safely tucked away in a bank account. This stash can help protect your household from sudden, unforeseen life events, like roof repairs or job loss. Keeping cash on hand gives you flexibility when life throws a surprise at you.

Awareness of Additional Fees

Changing your loan setup can trigger new appraisal fees or legal costs. You also need to budget for administrative fees if you plan to switch lenders. Our team can help you calculate all these small expenses, so you can decide your next financial move with confidence.

Comparison of Market Rates

Your current lender might simply mail you a standard renewal offer, expecting you to stay. But shopping around may help you find more competitive interest rates or mortgage features. Our mortgage brokers in Calgary can quickly line up a range of rate options to help you see all your options and save money.

Steps to Discharge Your Mortgage

Payout Balance Confirmation

You’ll need to request the exact final dollar amount from your current lender, which you can verify against your official mortgage statement. A delay of even a single day can change the total because many banks charge interest daily. You need to ask about these daily interest charges and send the funds so they arrive precisely on time.

Legal Help Requirements

You may need to hire a real estate lawyer to handle the final official paperwork. Depending on the lender and the type of payout, you may work with a real estate lawyer or notary to complete the final paperwork and mortgage discharge.

Property Title Updates

The registry office removes the lender’s name from your official property title. Once the discharge is processed, you should receive confirmation that the lender has been removed from the property title, either digitally or in the mail. With that document in hand, you can finally celebrate your brand-new status as a debt-free homeowner. Congratulations!

Managing Mortgage Renewal Together

Paying off your house loan can require precise timing and a clear understanding of the rules, but when you do it with an experienced team, it can feel much easier. At Mortgage Connection, we can help guide you through the entire renewal process. Reach out today to explore all available options for your upcoming renewal.