You might notice the value of your house going up over the years. This increase may mean you have equity tied up in your property, and many homeowners wonder whether it’s possible to access it for major renovations or to consolidate other debts. At Mortgage Connection, our mortgage brokers can help you understand how to unlock the value of your home without selling the property.

A home equity line of credit (HELOC) works as a revolving pool of money secured against your house. You borrow funds as you need them and pay interest only on the amount you actually use.

The Basics of a Home Equity Line of Credit

Think of this credit line like a flexible borrowing account tied directly to your property. You pull cash out to pay for a kitchen remodel, and your available limit goes down. Once you pay that money back, your full limit becomes available to use again. This flexible setup gives you more control over how much you borrow over time.

In Canada, many standalone HELOCs let you borrow up to 65% of your home’s value. If the HELOC is combined with your mortgage, some lenders may allow total borrowing up to 80%, depending on your financial situation.

Approval depends on factors like your income, credit history, current mortgage balance, existing debts, and the appraised value of your property. Our team knows how overwhelming this can be, which is why we’re here to help every step of the way.

Types of Home Equity Credit Lines

You have a few different options for setting up this type of credit line. Standalone HELOCs operate completely separate from your primary mortgage because they have their own account with a separate monthly statement and payment schedule. This works well if you want to keep your project funds clearly divided from your regular household expenses.

Other lenders offer HELOCs combined directly with your current mortgage. Your available borrowing limit grows automatically as you pay down your primary mortgage balance, which can be helpful if you want to keep all your home loans and borrowing in a single convenient place.

Requirements & Minimum Equity Needed for Approval

Lenders want to see a specific amount of ownership before approving your application. In Canada, homeowners generally need at least 20% equity in their home to qualify for a HELOC, which helps show the lender that you have a solid financial stake in the property.

The approval process involves a few specific steps to verify your financial health, including passing a stress test to prove your ability to handle future interest rate increases. The lender reviews how your current debt impacts the application, and they may order a fresh property appraisal to confirm the exact market value of your home.

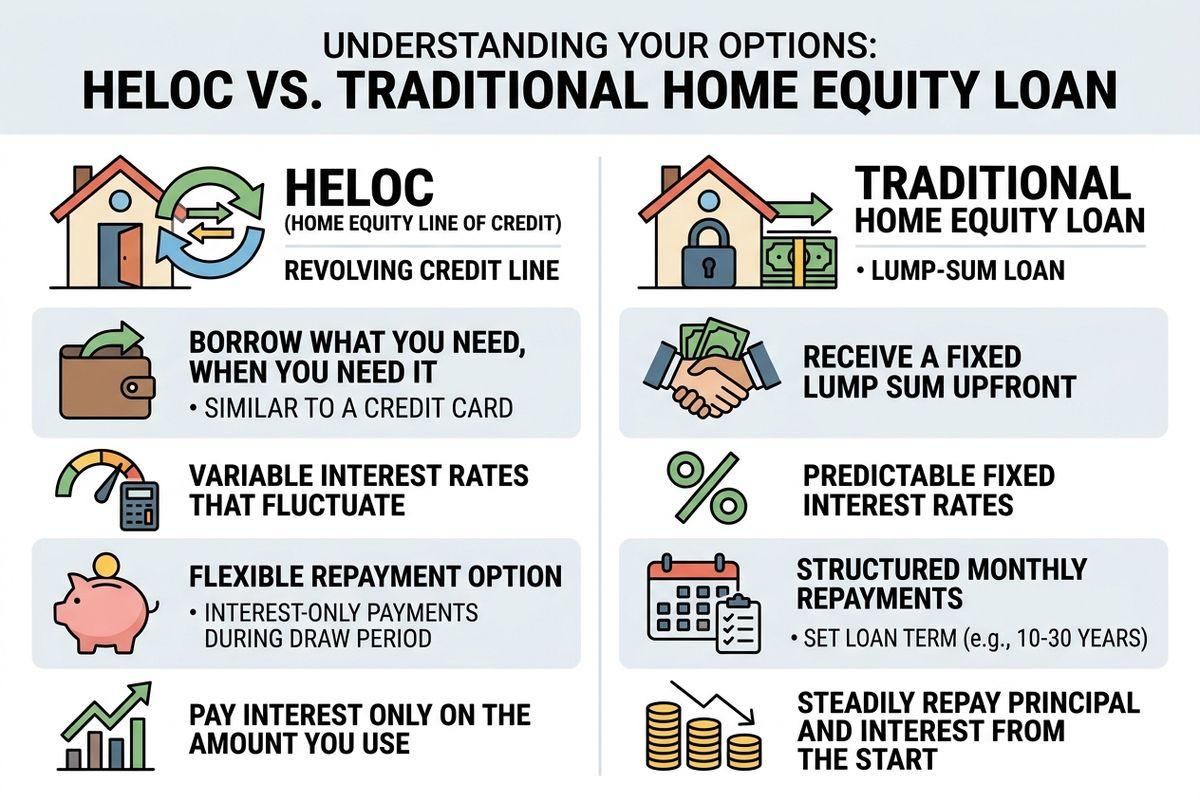

HELOC vs. a Traditional Home Equity Loan

How the Funds Work

The main benefit of a line of credit is the flexibility it gives. You can borrow and repay funds as needed over many years. This works nicely for long projects, such as financing home renovations, where you pay contractors in stages over several months.

Traditional loans provide a single large upfront cash payment instead. You receive the entire amount at once, and you start paying interest on the full balance immediately. This structure helps when you have a single large purchase to make.

Interest Rate Differences

Credit lines often feature variable interest rates tied to the prime lending rate. HELOC rates are often tied to a lender’s prime rate, which may change when the Bank of Canada adjusts its policy interest rate. Therefore, your monthly costs may go up or down based on these market shifts.

Traditional loans offer fixed rates instead, so you would be locked in a specific percentage for the entire term. This creates predictable monthly schedules to help you plan your household budget.

Payment Structures & Expected Monthly Costs

Managing your cash flow can be easier with flexible payment rules. With a HELOC, you pay only interest on the amount you actually borrow. So if you have a $100,000 limit but only use $10,000 to fix a roof, you pay interest on just that $10,000.

The exact cost depends on current interest rates and your unpaid balance. Payments on a $50,000 balance fluctuate as rates change in the market. You can estimate these costs by multiplying your current balance by your assigned interest rate.

Many HELOCs allow interest-only minimum payments while funds are outstanding, although borrowers can usually pay down principal at any time. Repayment structures vary depending on the lender and the type of HELOC product.

Key Considerations & Points to Review

Every financial decision comes with specific tradeoffs, and it’s always a good idea to review your long-term financial goals and plans before signing a contract.

When to Explore Other Credit Options

In some cases, a HELOC might not be the right choice for you. A sudden rate jump, for example, can make your borrowed money more expensive to carry, increasing the risk of financial strain or missed payments. Moreover, withdrawing cash affects your overall financial picture. You walk away with less cash if you decide to sell your house next year.

This is often why people decide to consult with a mortgage broker before making any decisions. Our team can help you understand your options in clear terms and make a decision based on your goals.

Your Next Steps

At Mortgage Connection, our team wants to help you review your current equity and borrowing options so you can feel confident in your financial options. Navigating property finance can feel much easier when you know you have an experienced professional on your side. If you’re curious about a HELOC, we encourage you to reach out to Mortgage Connection today to explore your next steps.