You finally found a house with everything you’ve wanted: A huge backyard for summer barbecues, a garage that fits your family’s skis, and space that feels inviting. You feel excited to start making it your own, but suddenly face a confusing wall of financial terms when it comes time to submit your mortgage application. At Mortgage Connection, we know how overwhelming this process can feel, but our team is here to help, so you don’t have to do it alone.

Mortgage underwriting is the formal review process where a lender checks your financial details to approve your home loan. This step helps lenders assess financial risk and confirm that the mortgage is appropriate based on your financial situation.

The Purpose of the Loan Review

A lender reviews your application to assess financial risk before granting final approval. They review your file to verify your identity, and they check your income stability and the source of your down payment. Our team of experienced mortgage brokers in Calgary can help break down the paperwork and explain these details so you understand the process every step of the way.

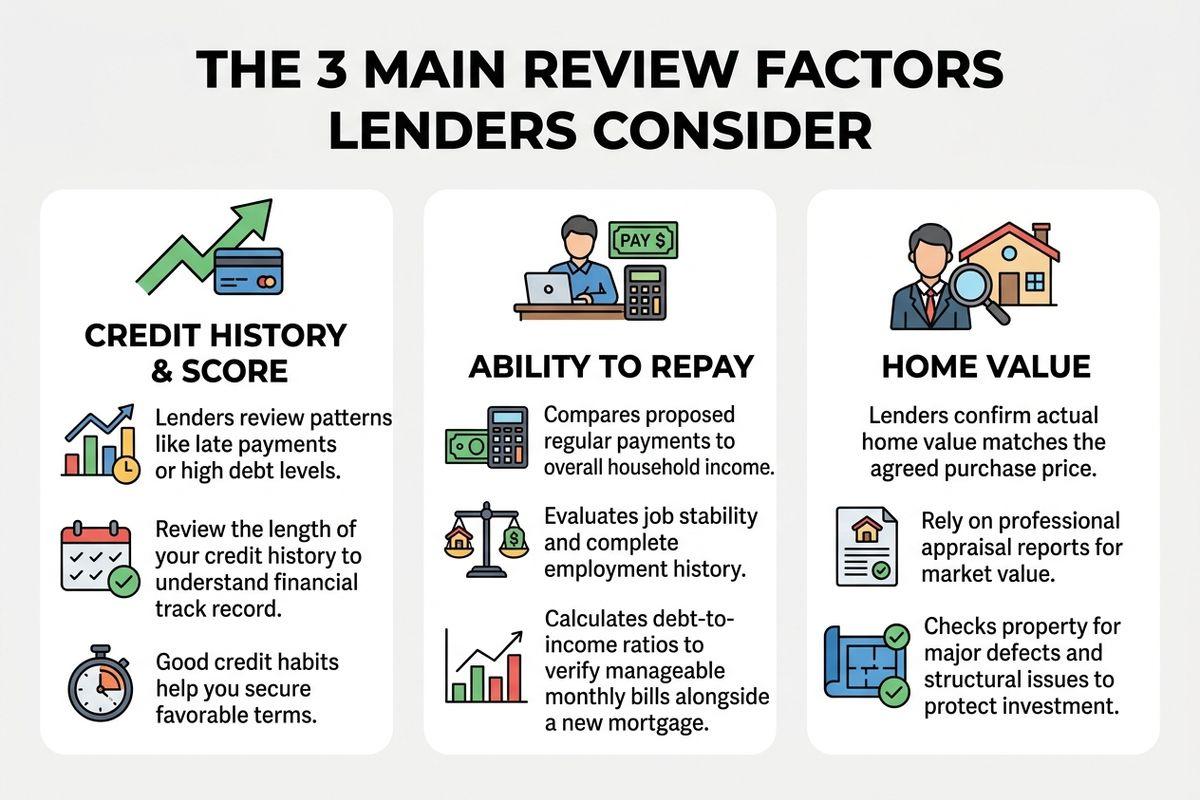

The 3 Main Review Factors

Credit History & Score

Lenders check your past loan repayment habits to understand your financial track record. They look for patterns like late payments or high debt levels on your existing accounts, and they review the length of your credit history to see how long you’ve managed borrowed money. Strong credit habits may help you qualify for more favourable mortgage terms.

Ability to Repay

The review team compares your proposed regular payments to your overall household income. They look at your job stability and your complete employment history over the past few years, and they calculate your debt-to-income ratios to verify that you can comfortably manage monthly bills alongside a new mortgage.

In Canada, many borrowers must also qualify under the mortgage stress test, which helps lenders assess whether payments would still be manageable if interest rates rise.

Home Value

Lenders want to confirm the actual home value matches your agreed purchase price. They use professional appraisal reports to determine the property’s exact market value and identify major concerns that could affect its value or marketability. This evaluation helps protect your financial investment over the years.

The Timeline & Review Steps

Paperwork Checks

The review team looks closely at your recent tax returns and bank statements. They’ll also trace your funds to confirm your down payment comes from a legitimate source. It’s a good idea to keep your paperwork organized at this stage so you can keep moving smoothly and avoid potential delays caused by missing documents.

Property Appraisal & Title Search

An appraiser visits the house to verify that the property holds enough value for the loan amount. A legal team also performs a title search on the property to look for any unpaid property taxes or existing legal claims on the house. Clear property titles help you avoid surprises on your moving day.

The Expected Timeline

The entire review process takes anywhere from a few days to several weeks. Missing signatures or incomplete forms often delay the final decision. You can speed up the review by sending prompt replies whenever the lender asks for more details. Quick responses can help prevent unnecessary delays in the review process.

Possible Decisions for Your Application

Final Approval

Final approval means the lender has accepted your application, and any remaining conditions have been satisfied, so you have the green light to move forward. You can then schedule your final home purchase date and start packing your boxes.

Conditional Approvals or Pauses

Lenders sometimes pause your application if they need a few more details. They might ask you to provide extra tax forms to clarify your income history. They also require you to buy property insurance before they finalize the paperwork. Handling these requests quickly can help get your application moving again.

Loan Denial

A lender sometimes turns down an application because of sudden changes in your employment or new debts. A low appraisal value may also create problems if the lender believes the property is worth less than the agreed purchase price. You can always reapply after adjusting your financial plans and building your savings. Taking time to pay down balances strengthens your profile for your next application.

Tips to Prepare Your Finances

You can take specific steps to strengthen your application before the review starts. A solid financial profile helps the lender process your file faster. We often recommend focusing on a few key areas to get your application ready:

- Avoid opening new credit cards or taking on car loans before you buy a home

- Save extra money in a dedicated account for your down payment and closing costs

- Organize 2 full years of tax documents and pay stubs, so you have them prepared

- Avoid major financial or employment changes during the mortgage approval process whenever possible

Your Next Steps

Navigating a mortgage application feels much easier when you have an experienced professional on your side. Our team at Mortgage Connection can help you organize your details, understand the process, and feel confident at every step. Reach out today to discuss your next property purchase and start your journey home.